Last Updated on April 11, 2024 by Chin Yi Xuan

Did you know? Depending on where you invest, a tax may be charged on your dividends!

Dividend withholding tax is something that most investors are unaware of when investing.

In this post, let’s learn about dividend withholding tax as a Malaysian, how it affects your investments, and what can you do about it!

Related Read:

- Singapore REIT ETFs overview: Earn dividends at 0% dividend withholding tax!

- Freedom Fund: My dividend income portfolio!

- My monthly dividend income update

p

Table of Contents

Highlights of dividend withholding tax

- Dividend withholding tax is a tax that investors incur while receiving dividends from their investments.

- Depending on what you invest in (stocks or Exchange-Traded Funds (ETFs)), the withholding tax rate will apply to you differently.

- Dividend withholding tax impacts each investor differently. In particular, dividend investors should be mindful of the tax when making their investment decisions.

What is dividend withholding tax?

Withholding tax is a method that a country uses to collect taxes from non-residents who have derived income from the country.

As an example, when we invest in stocks in a foreign country (eg. the US), the dividends that we received from our investments are usually charged with a withholding tax. To be precise, that’s what we call ‘dividend withholding tax’.

So, how does dividend withholding tax work? How does it affect us as an everyday investor?

Let’s find out!

How does dividend withholding tax work?

Depending on what you invest in, the way a dividend withholding tax will apply to your investments will differ:

Scenario 1: You invest in stocks

If you invest in stocks, your dividend withholding tax rate is determined by your country of residence.

Most of the time, the rate is determined by whether Malaysia has a tax treaty with the other country.

So, if you invest in US stocks as a Malaysian, you are charged with a 30% dividend withholding tax. If you invest in Singapore stocks, you will enjoy a 0% rate as a Malaysian.

Scenario 2: You invest in funds such as Exchange Traded Funds (ETFs)

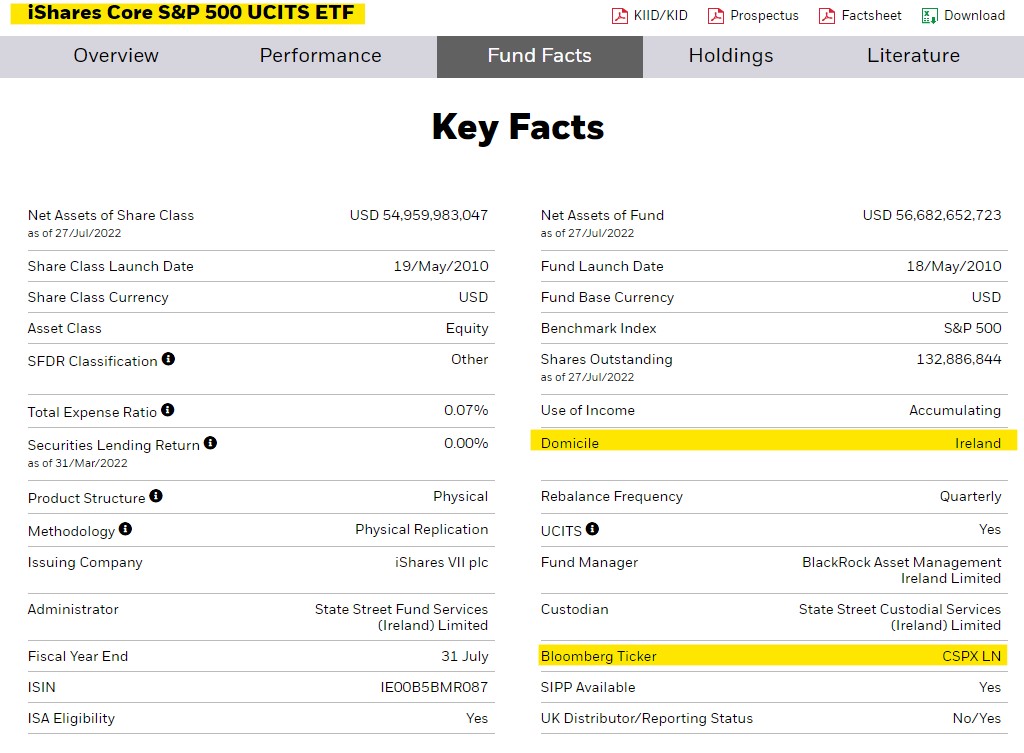

The dividend withholding tax rate of an ETF is determined by the country where the fund is domiciled in.

Simply put, ‘domicile’ refers to the country where a fund’s holding company is legally incorporated.

What’s the difference though? Glad you asked.

Essentially, not every ETF listed in a country is necessarily domiciled in that country.

For instance, Singapore has its own S&P500 ETF (which tracks the top 500 listed companies in the US) listed on its exchange, namely the SPDR S&P 500 ETF Trust (SGX code: S27). However, if you dig into the fund’s prospectus, you’d notice that S27 is actually a US-domiciled fund.

Hence investors of S27 ETF, regardless of country of residence, are subjected to a 30% dividend withholding tax.

Meanwhile, S&P500 ETFs such as CSPX and VUAA are Ireland-domiciled ETFs listed on the London Stock Exchange (LSE). Since Ireland has a tax treaty with the US, Ireland-domiciled ETFs are only subjected to a 15% withholding tax.

As a result, instead of investing in US-domiciled funds, Ireland-domiciled ETFs are usually the go-to choice for investors outside of the US to gain exposure to the US market due to favourable tax conditions.

READ MORE: Guide: How to invest in S&P500 as a non-US resident

So, how do we pay our dividend withholding tax?

Essentially, the dividend withholding tax is deducted automatically from your dividends BEFORE it is distributed to you.

As such, as a Malaysian, it is NOT compulsory for you to declare dividend income to LHDN again while filing for personal income tax.

As an example, Apple decides to pay out $0.10 distribution per share to investors. Let’s say you own 1,000 shares, you’d receive:

- Without dividend withholding tax: $100 in dividends ($0.10*1000 shares)

- With dividend withholding tax deducted (30% for US-listed stocks): $70 in dividends ($0.10*70%*1000 shares)

Dividend withholding tax rates for Malaysians

Below, you can find the dividend withholding tax rates relevant to most Malaysian investors:

p

| Country | Dividend Withholding Tax Rate |

| Malaysia | 0% (10% for REITs) |

| Singapore | 0% |

| Hong Kong | 0% |

| UK | 0% |

| China | 10% |

| Canada | 15% |

| Australia | 15% on unfranked dividends. 0% on franked dividends. |

| Japan | 15% |

| Ireland-Domiciled ETFs (London Stock Exchange) | 15% |

| US | 30% |

How does it affect you?

Dividend withholding tax affects investors differently.

-

Growth investing – minimal impact

If you invest in growth-related stocks or ETFs like Tesla and ARKW, the impact of dividend withholding tax is minimal.

The reason is, growth stocks do not usually pay high dividends (or they do not pay dividends at all).

-

Dividend investing – significant impact

As for dividend investors, it is essential to be aware of dividend withholding tax while investing.

Since dividends make up a significant portion of the overall return of dividend-focused stocks/ETFs, it is crucial to take into account the impact of withholding tax.

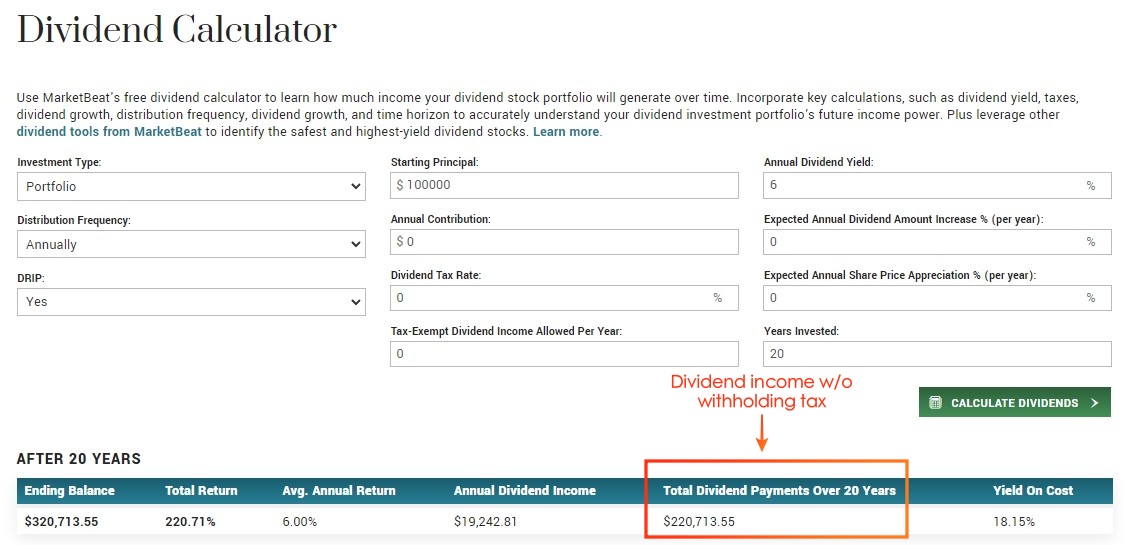

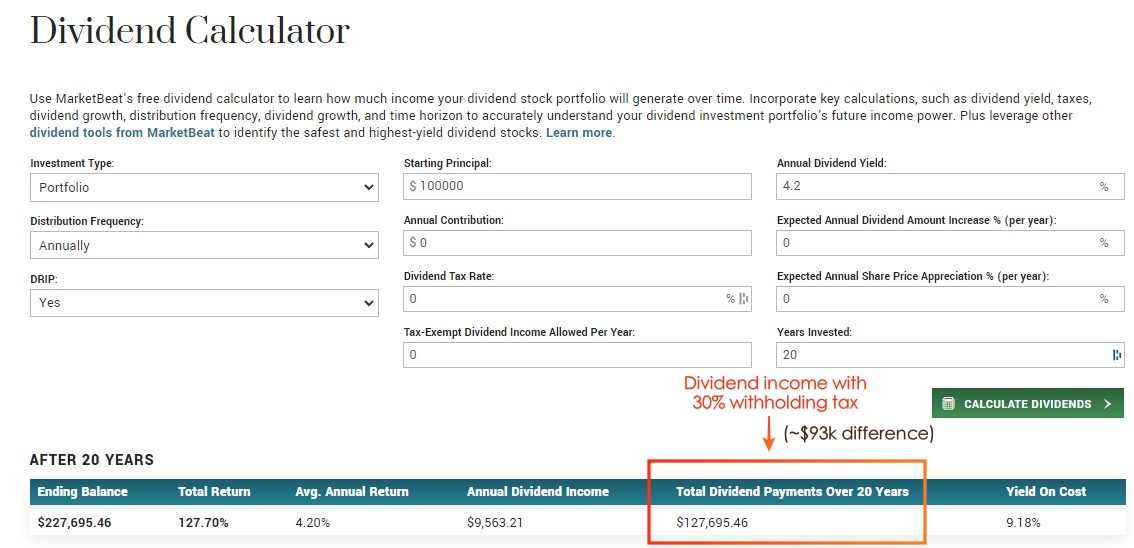

For instance, assuming you invest $100,000 in a US dividend portfolio that generates a 6% dividend yield annually. Below is the total dividend that you’d earn without dividend withholding tax (0%):

In this case, a 30% dividend withholding tax would cause you to end up with over 42% (~$93,000) less in dividend income over the span of 20 years!

In short, it is obvious that dividend withholding tax will impact the returns of dividend investors as a whole.

How to deal with dividend withholding tax as an investor

Usually, most investors would look to the US stock market while investing globally.

However, the 30% dividend withholding tax from the US can be very costly, especially to investors holding stocks where dividends form a significant portion of their returns.

Here are some of the things you can do to reduce the impact of dividend withholding tax on your long-term returns:

- Generally, avoid dividend stocks/ETFs that are listed or domiciled in the US. For ETFs, you can find out the domicile details on the official site or prospectus of the fund.

- Opt for stocks/ETFs that are listed or domiciled in markets with 0% withholding tax, such as Singapore and Hong Kong.

- Alternatively, you can also opt for Ireland-domiciled ETFs that are listed on the London Stock Exchange (LSE) or Canadian-listed stocks/ETFs, which are generally more tax efficient (15%).

Regardless of the market, ProsperUs by CGS-CIMB has you covered with access to 30+ stock exchanges (US, Hong Kong, China, Japan, UK, Singapore, Malaysia, Europe, and more!).

Check out my ProsperUs review HERE.

Side note:

With 0% withholding tax, the Singapore REIT market is one of the most established REIT markets in Asia, and it pays a decent dividend as well! Click HERE to learn more about Singapore REIT ETFs!

A word on tax on Foreign Source Income (FSI) for Malaysians

As of the production of this post, Malaysians are not required to pay any further tax on dividends received from overseas investments, aside from the existing Dividend WHT explained in this article.

That said, the government did propose to tax FSI in Budget 2022 (announced in 2021). This means when Malaysians transmit income back to Malaysia from overseas (including dividends), there will be a tax to be paid.

However, coming into December 2021, the plan (tax on FSI for Malaysians) is put on hold until 31st December 2026.

In short, for your overseas dividends, you are not required to pay any tax aside from the Dividend WHT mentioned in this post – at least until 2026.

Will any of these policies change (for the better or worse)?

Based on my understanding of the Malaysian government’s policy-making habits, I think it is hard to tell and I have zero control over this. So, I will focus on continuing to grow my dividend portfolio instead of worrying about the things that may or may not happen.

I will keep this section updated if there’s any news!

No Money Lah Verdict

I hope this guide has been clear and helpful!

I’ve received many tax-related questions on dividends in the past and I think we may have overcomplicated things due to a lack proper of information.

If you have any questions, feel free to let me know in the comments section below!

FAQ on Dividend Withholding Tax

Q1: As a Malaysian, do I need to declare my dividend income while filing for income tax?

No, you are NOT required to declare your dividend income while filing for personal income tax in Malaysia.

Q2: How do I pay for dividend withholding tax on my dividends?

You DO NOT need to pay for dividend withholding tax directly. Instead, they are deducted before your dividends are paid to you. In short, the dividends that you are receiving have been offset by withholding tax – there is nothing you have to do on your end.

Q3: Is dividend investing still a reliable approach with dividend withholding tax around?

Personally, I think dividend investing is still the most reliable way to build passive income. Meanwhile, dividend withholding tax is just part of the game, not a bug.

I will give additional thoughts into withholding tax while doing my research, but it will not deter me from building my dividend income portfolio!

Q4: What is the difference between ‘franked’ and ‘unfranked dividends’ for Australia-listed stocks/ETFs?

A franked dividend is a system set by the Australian government to eliminate double taxation in dividends.

As such, franked dividend is paid with a tax credit attached, where shareholders submit the dividend income plus the franking credit as income but will only be taxed on the dividend portion.

Meanwhile, unfranked dividends carry no tax credit. Since the company has not paid tax on the dividends paid, you will have to pay income tax on the particular dividend that you received as an Australian.

Looking for a reliable global broker? ProsperUs has you covered!

This educational post is sponsored by ProsperUs by CGS-CIMB.

ProsperUs by CGS-CIMB is a regulated broker from Singapore that gives investors access to 30+ exchanges in more than 8 countries. (US, Hong Kong, China, Japan, UK, Singapore, Malaysia, Europe, and more!)

Now that you’ve learned about dividend withholding tax, you have the choice to invest in countries with a more efficient tax rule via ProsperUs!

In addition, ProsperUs offers multiple instruments from stocks, ETFs, futures, options, Forex, and CFDs. This is great for investors looking to diversify across different asset classes.

Exclusive ProsperUs Referral Code – MONEY20

If you are thinking to give ProsperUs a try, here’s something exclusive to No Money Lah readers – you will not find this anywhere else!

From today till 30/6/2024, key in my exclusive promo code ‘MONEY20’ while you register, and get FREE cash credits up to SGD100 when you open a ProsperUs account:

p

| Tier | Initial funding within 30 days of account set up | Trades Executed | Cash Credits |

|---|---|---|---|

| 1 | Minimum SGD500 – SGD2,999 | Minimum 3 trades executed | SGD10 |

| 2 | Minimum SGD3,000 – SGD14,999 | Minimum 3 trades executed | SGD20 (Deposit SGD3000 or more), OR SGD20 + SGD30 (Deposit SGD3000 or more + Min. trades fulfilled) |

| 3 | SGD15,000 or more | Minimum 3 trades executed | SGD20 (Deposit SGD3000 or more), OR SGD20 + SGD100 (Deposit SGD15,000 or more + Min. trades fulfilled) |

Click HERE to view the full T&C of this referral reward.

Open a ProsperUs Account Today!

Disclaimers

This article is brought to you in collaboration with ProsperUs by CGS-CIMB.

Any of the information above is produced with my own best effort and research.

This post is produced purely for sharing purposes and should not be taken as a buy/sell recommendation. Past return is not indicative of future performance. Please seek advice from a licensed financial planner before making any financial decisions.

This post may contain promo code(s) that afford No Money Lah a small amount of commission (and help support the blog) should you sign up through my referral link

Hello Yi Xuan, thank you for the informative article as always. I have a question on Capital Gain Tax for stocks listed in Singapore. Do we (Malaysian) need to pay any tax in Singapore and Malaysia for Capital Gain made from Singapore stocks? I know we don’t need to pay for Capital Gain for US stocks.

Unless you make active income from the capital gain (ie. active short term trading), then no need.

Regards,

Yi Xuan