Last Updated on June 14, 2024 by Chin Yi Xuan

“What’s your investment strategy?”

This is a question I am often asked when talking to like-minded readers or friends in the investing community.

My answer? It depends on when you ask me this question.

In my early 20s when I first started investing, I did not have a specific style. It was an exploration phase for me, as I dabbled with different things (IPO, individual stocks) and was often influenced by my peers’ opinions.

As I turn 30 this year, I have managed to structure an investing strategy that fits my goals and lifestyle.

Simply put, going through several life-changing events and figuring out my priorities have inspired me to reflect on the investing strategy that suits me the most.

Read on as I’ll cover this topic in detail.

Table of Contents

Overview: My journey in discovering my 2 investing strategies

Before coming to my present style, I have tried different things. Here are 2 things that I have either cut down, or stopped doing entirely:

- Investing in individual stocks & REITs: I still do so right now, BUT I have reduced my holding on individual stocks or REITs as I do not have time to research individual companies.

- Shorter-term stock trading: I’ve stopped mixing short-term stock trading with my long-term investing strategy. Rather, to explore my interest in trading, I joined a proprietary trading firm last year (2023) to develop my trading career in the futures market (instead of the stock market). For me, short-term trading is a career, investing is a routine – they have to be done separately.

With that, I have come to 2 of my current investing strategies: Dividend and growth investing.

My investing strategy #1: Dividend investing

Long-time reader would know that I share my dividend portfolio (ie. My Freedom Fund) and dividend income on this blog.

Why dividend investing?

There are a few life-changing events in my 20s that led me to commit to dividend investing eventually:

- Cashflow as a self-employed:

- In the early years of my career, without a consistent cashflow, planning long-term business & life decisions were difficult as I would be forced into survival mode. As a self-employed, building a steady cashflow is my most important financial measure in business and life.

- Aging parents:

- A key incident in my 20s was my late grandmother being bedridden. In this incident, my family & relatives were caught off guard by the expenses & energy required to take care of her. As such, I’ve learned about the importance of having a low-maintenance passive income so I can focus on people/things that matter without the money anxieties when the time comes.

How do I do dividend investing?

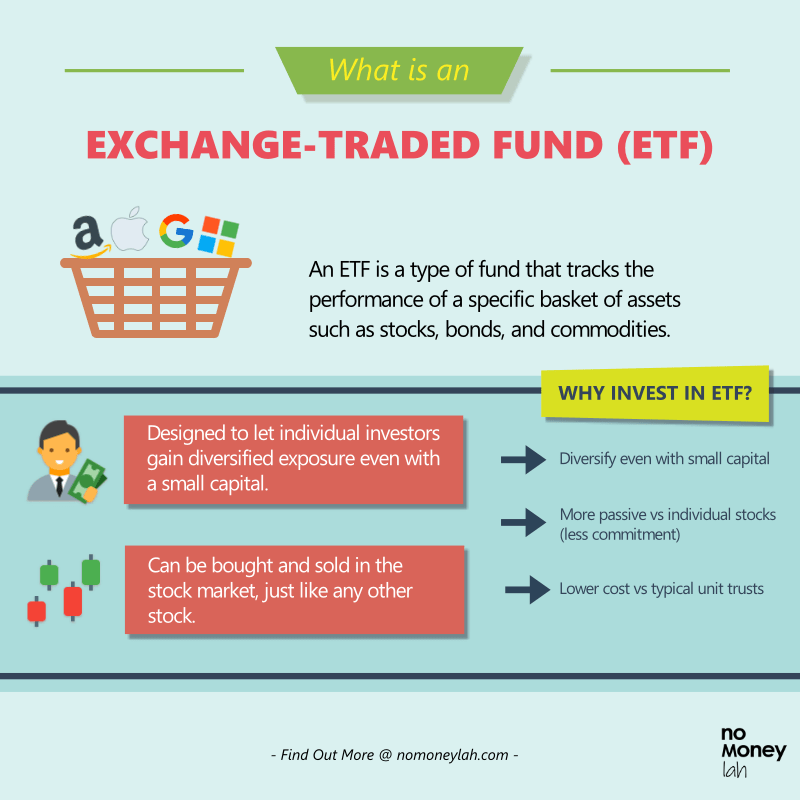

Generally, my Freedom Fund involves investing in Exchange-Traded Funds (ETFs) that pay dividends.

To expand further, there are 4 types of dividend-paying instruments in my Freedom Fund:

- Dividend growth ETF: ETFs that grow their distribution consistently. So I get paid more each year as I hold these ETFs for the long term.

- Covered call ETF: ETFs that employ covered call options strategy in all or part of its underlying asset. This allows covered call ETFs to generate extra premiums in addition to the dividends from the underlying stocks – resulting in higher distribution.

- Individual REIT or REIT ETF: Exposure to commercial real estate which generally pays decent dividends.

- Individual dividend stocks: Individual stocks that pay attractive dividends. This is a smaller part of my portfolio as I do not enjoy researching individual stocks.

Check out what’s in my Freedom Fund below, or click HERE for more detailed breakdown.

What is my goal for dividend investing?

With dividend investing, steady cashflow is my primary goal. I have a pretty clear timeline of about 15 – 20 years. By this time, I’d be in my mid or late 40s, where I foresee the need for steady dividend income (ie. cashflow) in scenarios where my parents may require additional care, or if I have my own family of which I’d like to spend more time together.

Moreover, having a steady dividend income that can pay for my expenses also means more choices and authority to do whatever I want, be it a short break from work, or a long vacation.

Simply put, my dividend income will give me the freedom of choice to focus on things that matter.

My investing strategy #2: Growth investing

Growth investing is also another investing style that I do in parallel to dividend investing.

Generally, investments in growth assets pay little to no dividends. Rather, most returns of growth investing come from the appreciation in value of the assets.

Why growth investing?

My goal for growth investing is to prepare for my older days. If I were to put a rough timeline, it’d be about 30 years, of which I’d turn 60.

As such, with about 30 years in mind, my goal is to invest in assets with a strong tendency to grow in value over a long time frame.

How I do growth investing:

There are many ways to do growth investing. Some may prefer to research and pick individual stocks with growth potential.

For me, I do not prefer picking individual stocks. As such, investing in Exchange-Traded Funds (ETFs) is my go-to alternative.

Every month, I will do a routine Dollar Cost Average (DCA) on my growth portfolio regardless of market condition, as I believe my entry price will average out over time.

READ: Click HERE to check out my guide to Exchange-Traded Funds (ETFs)

What’s in my growth investing portfolio?

Briefly, the main investments in my growth portfolio are:

#1 S&P500 ETFs (CSPX, VUAA):

At ~12.5% annualized return for the past 10 years, ETFs like CSPX and VUAA are Ireland-domiciled ETFs that track the performance of the S&P500 index, representing the largest 500 listed companies in the US.

This is also the largest holding in my growth portfolio.

Check out my full guide on how to invest in S&P500 HERE.

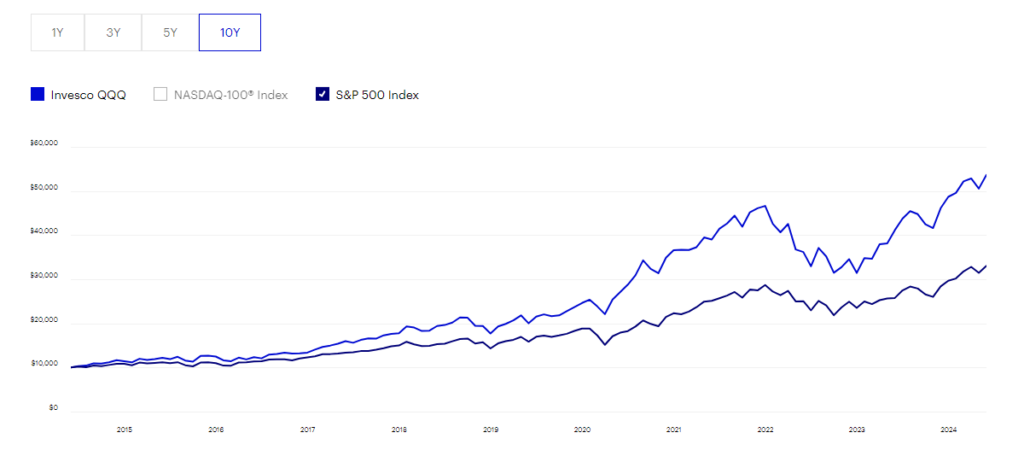

#2 Tech sector ETFs (QQQ, XLK):

At ~18% annualized return for the past decade, QQQ and XLK are ETFs that track, or with exposure to the overall US tech sector.

Generally, tech-focused QQQ and XLK tend to outperform the S&P500, but also experience more volatility and larger drawdown during a downturn. This is the 2nd largest holding in my growth portfolio.

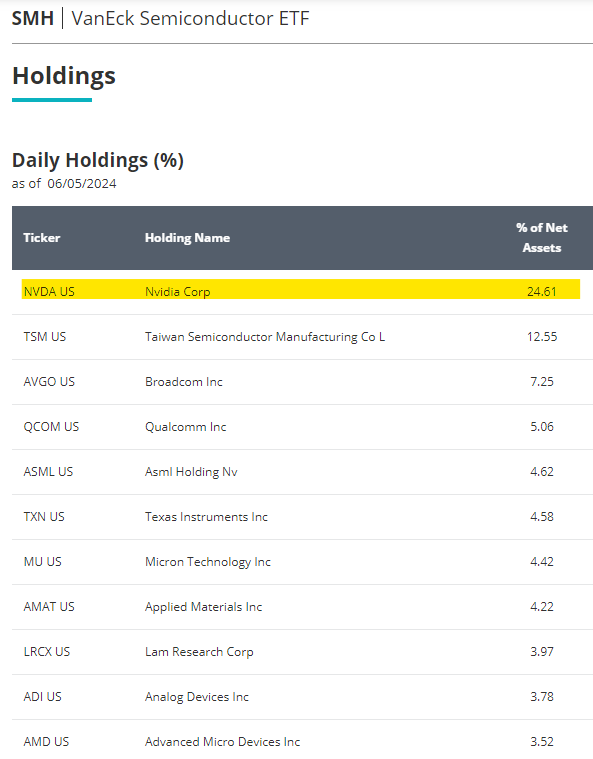

#3 Semiconductor ETF (SMH):

At ~27% annualized return for the past 10 years, the VanEck Semiconductor ETF (SMH) is an ETF that tracks the overall performance of companies involved in semiconductor production & equipment.

In other words, by investing in SMH, you’ll get exposure to companies like Nvidia (NVDA), Advanced Micro Devices (AMD), and Intel.

Since I think AI development is going to be the focus for the coming decades, investing in SMH will give me the extra boost I need to grow my wealth.

#4 Crypto: Bitcoin and Ethereum

The next in my growth portfolio would be major cryptocurrencies like Bitcoin and Ethereum.

As a whole, I’d like to keep things simple when it comes to investing. As such, I adopt a hands-off approach by consistently investing a specific amount to my growth portfolio every month.

Other investing vehicles

Aside from my main portfolios, I also invest & contribute to things like:

- EPF & PRS to maximize tax relief

- ASNB

- Gold

- Robo-advisors like StashAway, Syfe, Wahed, and Versa Invest.

My investing timeline

The timeline for both my investing strategies are different and fulfill a specific role:

What to consider while designing your investing strategy/style

How you should invest depends largely on your personal circumstances and goals in life – there is simply no one-size-fits-all investing strategy.

4 things to consider while determining how you should invest:

Factor #1: Career and income stability

The state of your career and income can be a factor to consider.

For instance, being a self-employed, I am aware that my income may not always be steady. Hence, I have chosen to commit to dividend investing to build consistent cashflow as a financial measure in the future.

Meanwhile, one with a more stable job and income (eg. you work in the government sector) may consider focusing purely on investing in growth assets to maximize their wealth.

Factor #2: Lifestyle & goals

The lifestyle and goals you are looking to pursue are important factors to consider as well.

Some invest to live a rich life one day (eg. expensive cars, luxury bags). I invest to live a financially free life.

To live a rich life means you will need a lot of money to do so. But to live a financially-free life can be done even without a lot of money.

For instance, if I only need RM5,000/month to live comfortably, then I am financially free to moment my passive income from dividends reaches or exceeds RM5,000.

Therefore, it is important for you to be clear about the life you’d like to live.

Factor #3: Time to manage portfolio

Not everyone will have the time and find it fun to actively research and manage their investments.

I am one of those people, which led me to incline towards investing in ETFs which I consider low maintenance.

What do I use to invest?

Personally, I use multiple platforms to invest, as a way to diversify my funds.

#1 Global stocks & ETFs (US, London, Canada): Interactive Brokers (IBKR)

Interactive Brokers (IBKR) is my go-to platform for global stocks and ETFs as it provides access to over 150 markets in 34 countries, including the US, UK, and Canadian stock markets which I need to build my portfolio.

Furthermore, IBKR has one of the most affordable fee structure in the market.

READ: Check out my Interactive Brokers (IBKR) review HERE.

#2 US and Malaysia stocks: Moomoo MY & Rakuten Trade

Aside from that, I also use locally-regulated platforms like Moomoo MY and Rakuten Trade to access the US and local Malaysia stock market.

READ: My in-depth Moomoo MY review

READ: Rakuten Trade long-term user review

#3 Robo-advisors: StashAway, Syfe

Aside from brokers, I also use robo-advisors like StashAway and Syfe to automate a lot of my investment routine.

For instance, I have automated monthly investments to Syfe’s Equity 100 ETF and REIT+ portfolio. I also use StashAway’s Flexible Portfolio for my smaller investment routine (eg. Investing for long-term family fund).

READ: My StashAway review

READ: My Syfe review

#4: Crypto: Luno

When it comes to investing in crypto like Bitcoin and Ethereum, my go-to platform would be Luno, since it is regulated in Malaysia and I have been using it since 2017.

Invest in crypto via Luno – use my dedicated promo code ZKQST, and you will get RM75 worth of Bitcoin when you invest RM250 or more.

No Money Lah’s Verdict:

I started dabbling with various investment instruments since my early 20s.

As I go through different life events and career progress in my 20s, I finally have a clear goal towards investing, as I discover what is important to me in life.

My biggest lesson from the past decade is there is no perfect investing style that can fulfill everyone’s need. It is a journey of discovery – your goals, your risk appetite, your capital – that determines how best to invest your money.

May this post helps you to reflect on your own investment style – stay awesome!

Disclaimers

Past performance is not indicative of future performance.

This post is produced for general information purposes only. It is not intended to constitute professional advice, and should not be relied on or treated as a substitute for specific advice relevant to particular circumstances.

The inclusion of Interactive Brokers’ (IBKR) name, logo or weblinks is present pursuant to an advertising arrangement only. IBKR is not a contributor, reviewer, provider or sponsor of content published on this site, and is not responsible for the accuracy of any products or services discussed.

The inclusion of Moomoo MY and Rakuten Trade’s name, logo or weblinks is present pursuant to a collaboration arrangement only. Moomoo MY and Rakuten Trade is not a contributor, reviewer, provider or sponsor of content published on this site, and is not responsible for the accuracy of any products or services discussed.